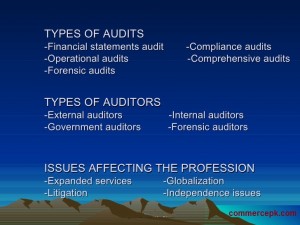

Types of Audits :

There are many types of Audits but here we will discuss the basic three audit types are as follow:

1. Final Audit

2. Interim Audit

3. Continuous Audit

Types of Audits methodology will discuss one by one.

1. Final Audit:

It is a types of Audits also known as periodic audit or complete audit or balance sheet audit. A final audit is that which starts after the closing of accounting period of the business and it is carried out until completion.

This is the most satisfactory types of audits from auditor’s point of view and is usually adopted where practicable particular in the case of small concern however in the large business a final audit is rarely applicable.

According to the companies ordinance the desired procedure for and auditor is to conduct an audit is final audit it is also called “complete audit” because t is conducted after the completion of accounting books and no transaction is allowed to entreat the end of financial year it is called “periodic audit” because it Is conducted after the completion of accounting period it is also called “Balance Sheet” audit because when the balance sheet is prepared completely it is conducted.

You may also like to Read

Advantage of Final Audit:

The advantages are as follow:

1. Facts:

All the information related with the books of accounts are supplied to the auditor with the facts relating to the year ended as an auditor can carry out his work with the help of full fact provided to him without any break through.

2. Work continuity:

The auditor will leave the work until and unless the audit is completed and moreover the final audit is conducted once in financial year therefore the work of management as well as the auditor not influenced.

3.Annual reports:

It very easy for the auditor to complete their work and report and present to the shareholders as easy as possible.

4. Less chances of alteration:

In this types of audits there is less chances of manipulation and alteration of figures they have been checked.

Disadvantages of Final Audit:

the disadvantages of this types of Audits are;

1.Alteration of figures:

There is possibility of alteration in figures either ignorantly or deliberately after they have been checked by an auditor.

In this way error or frauds cannot be detected without further rechecking.

2.Expensive:

This type is comparatively more expensive as the auditor takes several visits to perform his work.

Interim Audit:

The 2nd types of audits it refers to and audit conducted on a particular date with in an accounting period it lies midway between final audits and continues audit.

LR Howard Defines interim audit as “this is when an audit is conducted to a particular date within the accounting period is called interim audit.

It is not the usual way of audit it is just for exceptional cases where need arises. The purpose of interim auditing may be the declaration of interim dividend by a public limited company or in case of partnership when new partner want to come in or go out.

An audit which is take place between the two annual audits to find out the interim audit it is some in the particular period of the year.

Advantages of Interim Audit:

1. Interim dividend:

It is conducted to declare interim dividend the management can prepare the interim account for dividend purpose the shareholders feel satisfaction over the business concern.

2. Location of fraud:

In this types of audits fraud can be located due to interim audit the time between compiling and checking account is very short the location of fraud is possible as sufficient time is not given to employees.

Disadvantages of Interim Audit:

1. Figures alteration:

The limitation is that the accounting staff can alter figures after the completion of audit.it creates confusion in the minds of audit’s staff at the time of final audit.

2.Expensive:

The limitation of interim audit is that it increases the business expenses such audit is not computing it is optional for management and so audit fee is an extra expense for business.

Continuous Audit:

The 3rd Types of audits is also called “Detailed” or “Running Audit”.

It means that continues audit continues in the whole financial year final audit starts when financial year ends but continues audit is completely reverse the accounting process continues and side by side the audit is also done.

Under such types of audits the auditor has to visit the business house at interval during the financial ear the interval may be for a month a week or for some days so the process of auditing is continuous audit.

It depends upon the volume of organization and the matters of the business however there is no prescribed rule for the auditor that he follow the rule of time strictly usual the regular interval are follow.

LR Howard says that continues audit work is conducted throughout the course of financial year but is not taken at a specific accounting period as interim audit.

Advantages Continuous Audit :

The advantages of this types of audits are;

1.Easy rectification of errors :

As basis are checked soon after the entry has been passes, errors can be spotlighted as we as rectified quickly.

2.Special attention:

In this types of audits Before the finalization of accounts an auditor has sufficient time to give pepper attention for checking the account defects and locates the errors made intentionally.

Disadvantages Continuous Audit :

The disadvantages of this type of Audit are;

1. Figures Alteration :

There is possibility of alteration in figures either ignorantly or deliberately after they have been checked by auditor. In this way errors or fraud cannot be detected without further rechecking.

2. Inconvenience:

The frequent visits by an auditor and his frequent checking may dislocate his client so work and cause inconvenience to him the thread of work is also likely to be lost.