What are the Costs?

The costs correspond to all the costs incurred by the company during the whole process of production of a good or service.

Characteristics of Costs

Costs refer to all costs and expenses incurred by a company in the process of producing a product or service dedicated to sales. The activities of the company require a certain number of resources, for example, financial or human, which are considered as costs. A cost can be a cost price, a purchase cost, or a cost of production for example.

This term is used in management accounting (or cost accounting).

You may also like to read

The different Types of Costs

There are 4 types of costs: fixed costs, variable costs, direct costs and indirect costs.

The Fixed costs

are expenses that do not change depending on the activity of the company, for example, the rent or insurance.

The Variable costs

are expenses that vary depending on the activity of the company, such as transportation costs, energy costs (gas, electricity).

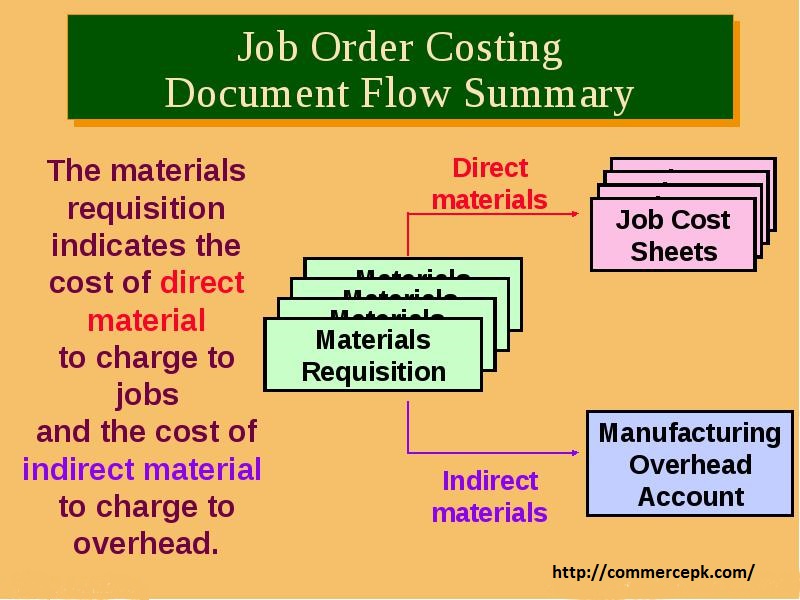

- The direct cost refers to the raw materials used entirely for the production of a specific property, such as labor.

- While an indirect cost corresponds to an essential burden for the production of several different goods, for example, administration, marketing, or rental of premises.

Methods of calculating costs

There are many different methods, but here are the main ones:

Variable Cost Method

This method is based on the distinction between fixed and variable charges. It is also possible to calculate the margin on variable costs to know the profitability of a product.

Full cost method

This method is based on the distinction between direct and indirect costs. It makes it possible to calculate costs such as the purchase cost.

Specific cost method

This method includes variable charges plus directly fixed charges. It excludes indirect elements. The specific cost is calculated as follows: Variable Cost + Indirect Fixed Cost.

It allows calculating the Margin on specific costs (Sales price - Unit specific cost).

Activity-Based Costing (CBA)

This method is based on the concept of activities within the company, not products. These activities require the consumption of resources.

If the company is therefore divided into activities, the units of work are replaced by “inductors”. For a specific activity, it is, therefore, necessary to calculate a number of inductors used.

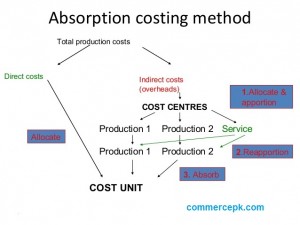

Direct and Indirect costs

In accounting, the direct and indirect costs are usually classified according to whether they are directly or indirectly due to the production of a given good or service.

The costs refer to all costs and expenses of a business. A distinction is made between direct and indirect costs.

A direct cost can thus mean the raw materials used wholly for the production of a single good, whereas an indirect cost may correspond, for example, to a charge necessary for the production of several different goods.

The direct costs are thus attributable to the production of a given good or service, without the need for any particular calculation. Regarding indirect costs, on the other hand, it is necessary to calculate what part of these costs should be charged to a particular good or service.

Indirect costs

The following is a list of examples of indirect costs found in most business accounts:

- Wages,

- Rent of commercial premises,

- Computer and telephone equipment,

- Advertising and marketing.

These are therefore necessary elements on a daily basis to ensure the smooth functioning of the company.

However, it is not possible to allocate them directly to the production of a unit (good or service) without a prior calculation.

For this purpose, the concept of imputation is used, which consists of typically flat-rate distribution keys: for example, the time of use of the machine for the production of an asset, the number of hours of labor essential to Produce a service, etc.

Direct costs

Direct costs are much simpler to calculate because they do not require allocation keys. Here is a list of direct costs:

- Given quantity of raw material entering into the production of a good,

- A number of hours of labor necessary to produce a specific service.

- The imputation of these direct costs is easy to achieve since the cost of producing a given good or service is known precisely and immediately.

There are, however, other ways of distinguishing costs. If we just see the difference between direct and indirect costs, we must also know how to differentiate the fixed costs for variable costs.